Seed Stage Risk is Gorgeous

Seed stage VC as an asset class offers something that is extremely rare: truly uncorrelated returns.

A well constructed portfolio is a set of investments each promising high returns relative to its risk and each taking different kinds of risk. Ideally, every investment would have unique risks.

In practice though, a perfect portfolio is impossible — investments with completely distinct risks don’t exist. They almost always share certain common ones. These are “betas” in allocator parlance and they are often but not exclusively tied to macroeconomic factors.

Capable allocators will understand the “net” beta risks they have in their portfolios and will actually be deliberate about construction to achieve the beta exposures they want. But they will do more than just that. They will also seek investments that promise high returns while taking something other than beta risks; they will seek uncorrelated returns aka “alpha”.

Uncorrelated returns are as difficult to find as they are delightful. They are difficult to find because beta has a nasty tendency to permeate almost any investment you can find. (A new generation of asset allocators “discovers” this every cycle. “OMG, the correlations all went to 1!”)

They are delightful because, when you actually find them, they won’t fail you when everything else does. They actually deliver what diversification promises. If you can truly find investments with uncorrelated returns – alpha – you make your portfolio better, possibly much better.

This brings me to the risk profile of early stage VC investing. If you are an investor who is truly seeking the nirvana that is high expected returns and diversification, early stage VC investing looks gorgeous to you. It looks gorgeous because it has essentially zero beta risk. The risk you take with early stage VC is real and substantial but it is truly unique. It is truly uncorrelated. It’s one of the few investments you can make that can really be “pure alpha”.

To see why, take a close look at the nature of early stage startup risk. Consider any particular freshly founded company. This fledgling enterprise might have a few hundred thousand dollars in funding, one or two founders and maybe an employee or two. Their 10 year mission: disruption, domination and eventually unicorn status climaxing with a massive IPO.

But that’s ten years from now. The current mission is far less glamorous: survive. On the ground that translates into working zealously so that the company can do something now that is impressive enough to secure more funding. It’s conceptually simple and extremely hard.

With fresh funding comes a new existential milestone and the cycle repeats. Many startups are in “survival mode” for years before they die or break out. Getting beyond the “just survive” stage to a point where there is a real product with real customers and real growth potential is extremely difficult. There are so many ways to fail. Risk factors like: the founders don’t have what it takes or the company gets out competed by another startup or the company’s tech isn’t good enough or there is just no product-market fit. The list is huge.

But here’s the key observation. This long list of startup risk factors is notable for what is not included. On this list you will not find non-farm payrolls or the price of oil or CPI or tariffs. Sure, one day the company hopes to be exposed to many of these beta risks. But not today. Not now. Early stage startup risks are different. They simply have no significant exposure to any traditional risk factor. With early stage startups the risk is all too stark, but it’s alpha risk, not beta risk.

I can make this point more tangible with an example. Often the milestone a fledgling startup faces is one of achieving what Peter Thiel called the “zero-to-one” transition. The existential mission that will determine if they get funded or not reduces to getting a customer. (If you haven’t tried to get a first customer for a product that didn’t used to exist, you simply cannot appreciate how hard this is to do. Which is why achieving zero-to-one is often sufficient to convince a VC to write a check.)

Achieving zero-to-one is so hard that most startups never actually do it. But here’s the thing: your success on this mission will simply not be affected by the overall state of the economy. If you have really invented a product that has value you can get a single customer no matter how bad the economy might be. In a way it is merciful that “all” you have to do is get one customer1. And that is what makes you immune to beta.

Contrast this with a larger company like a growth stage startup with $5 million in revenue that has to double that number in two years. This company can’t escape beta risk. They have to do $5 million in new sales in 2 years. That’s somewhere between 50 and 50,000 new customers depending on the price of the product. There is no way that mission is not exposed to the health of the economy. They’ve got beta risk.

Conceptually, here’s how beta risk looks as a function of a company’s maturity:

It’s only when you are truly fledgling that you are immune to beta risks. But there is no free lunch of course: you are excused from beta risk, but you still carry (large) alpha risk. That risk is so big that most companies will succumb to it.

One interesting aspect of this is perspective. The uncorrelated nature of startup risk does nothing for the founder. They are taking career risk and the fact that their initial survival will be uncorrelated to the S&P 500 doesn’t help them at all.

And even the early stage VC that backed them doesn’t care about this lack of beta risk. They need many of the companies they seeded to actually survive if they want to survive. The true beneficiaries of this lack of correlation are the LPs whose allocation to an early stage VC will have a fantastic diversifying effect on their portfolio.

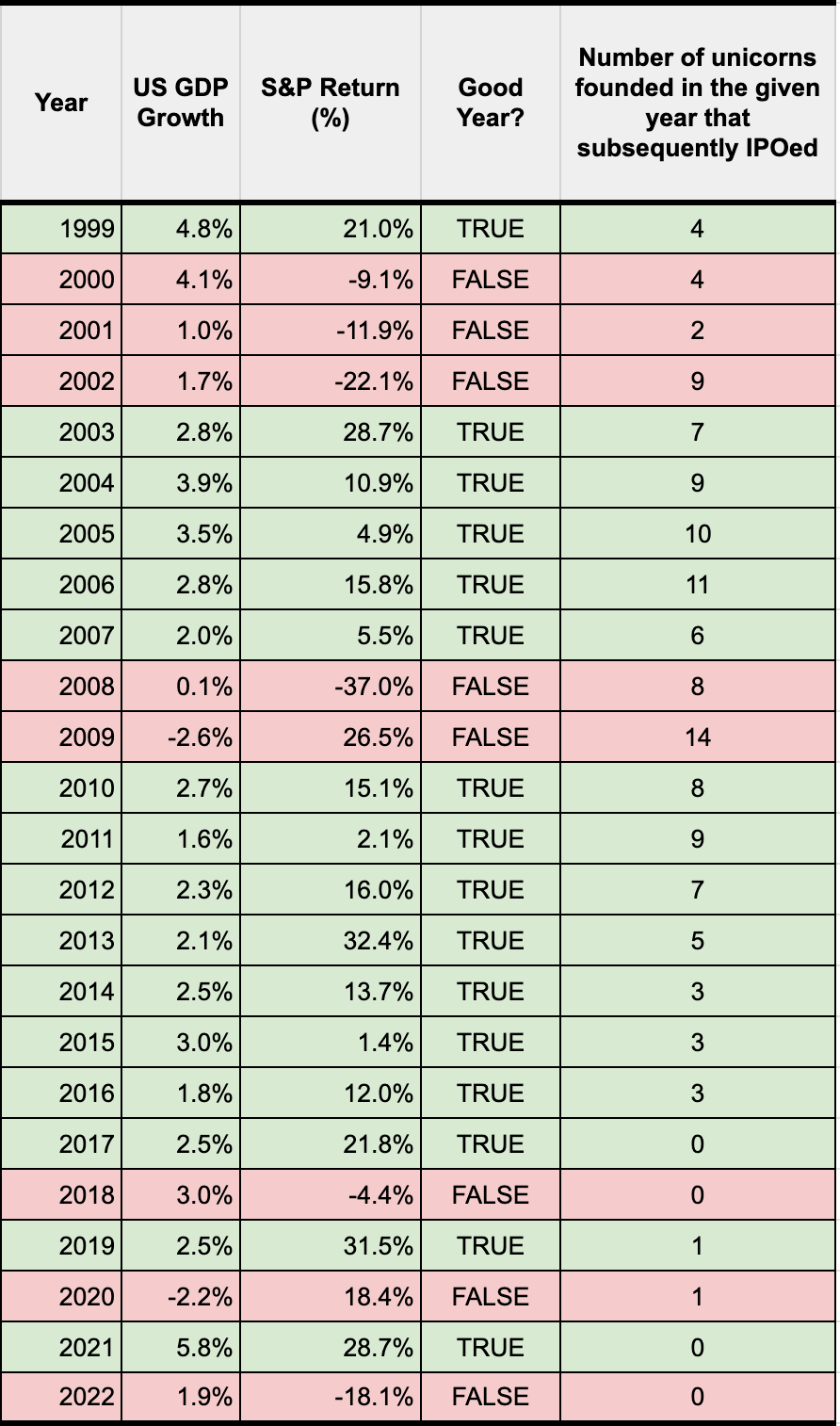

So that’s the theory. Is there a way to verify this presumed lack of beta with empirical data? One approach is to take a set of unicorns and look at when they were founded. If economic conditions at inception were important, one would expect that a disproportionately large number of unicorns were born during healthy economic times versus during recessions or stressed markets.

If we define a “good year” as one where US GDP growth is positive and the S&P 500 is up, then there are 16 good and 8 bad years between 1999 and 2022. There were 1242 tech unicorn IPOs during that period. Of those, 38 were born in “bad” years and 86 were born in “good” years.

Notice: two thirds of the years are “good” and two thirds of the unicorns were born in “good” years. One third of the years were “bad” and one third of the unicorns were born in “bad” years. In other words, there is no statistical evidence that startups born in “bad” times are any less likely to reach unicorn status versus any other time.

The empirical evidence can be underscored with some anecdotal sprinklings: Square, Twilio, Match, Sendgrid, Cloudflare, Bilibili, Cloudera, New Relic, Pure Storage, PagerDuty, Slack, Uber and Rivian were all born during the global financial crisis.

So data does indeed affirm what theory suggests: early stage VC is a near perfect investment with respect to its risk characteristics.

Early stage VCs succeed if they are seeding unicorns. (And fail if they’re not.) If unicorns are not being born, it’s a bad time to invest in early stage VC. And there may well be conditions that are unfavourable to unicorn birth rates but economic conditions are not one of them which is why seed stage risk is gorgeous.

Depending on the nature of the business, thresholds might be more than 1 customer. If your product costs $5, clearly you’ll have to do a bit better than that to achieve 0 to 1. But the point is, the threshold is low. (Don’t mistake this for easy.)